With the trends for 2017 out from most of the more professional outfits, it’s time for me to bring my predictions and thoughts to the fore. Of course, there will be no mention of #millennials #tech and #wearables and it’ll be a steely focus on the reality facing people this year.

The #future #trends are best left to those people who spend their time going to the Expo’s and talking incessantly about how the industry will continue to change and how this (being an entirely self service store) is the latest ‘big thing’.

The main talking point of the Sainsbury’s ‘food dancing’ campaign was that Spotify integration is ‘cool’, and how we should be mightily impressed with the wider work. Marvellous I’m sure – but how does anything related to that campaign, in stores, then translate into sales through the checkout?

Surely any marketing campaign is centralised on increasing footfall and sales to the business, otherwise what’s the point? Agencies would be well served to remember that the industry is still about sales in supermarkets. Not just Twitter, retweets, Facebook shares, gifs and social media scores.

The customer is often spoke about lustily by retailers and other industries that service the sector, did anyone ask customers for their input / thoughts on this campaign?

Anyway – my trends won’t be #wow trends or indeed ‘pie in the sky’ ideals. After all, the market is changing rapidly but the fundamentals of the industry remain the same as they ever were.

Goods are still delivered by road to shops and the vast majority of shopping still takes place in physical supermarkets that requires humans to be in place to serve customers and replenish the shelves.

Selling good quality food. At the right price for producer and customer. (and of course the retailer).

Food retailing is a simple business, in far from simple times – that’s a wider theme for 2017….Geo-political challenges are the norm for any market, particularly food given regulation and legislation. But this year will be extreme in the challenges it brings with economic instability impacting food prices.

The focus has to be on the customer, always. These 2017 trends will be different in that they consider the customer at large and what will shape their spending, thus the winners and losers in the market (based on the entwined efforts of the retailer themselves of course.)

What isn’t focussed upon here are the 3 customers who bought and wore the Google Glass image taking eyewear, because it happens to be cooler than talking about a reality for customers who face a day to day struggle to afford food, pre inflation, let alone post inflation 2017.

1. #Brexit

You cannot mix business and politics, well until Donald Trump came along and even then… It’s unclear just how his administration will pan out, nor can you predict just how Brexit will impact with so much talking and guesswork having gone on, all before article 50 is even triggered to enable the departure of Britain from the European Union. I don’t personally like talking politics in a business capacity but political landscape has made it a necessity given the events of 2016.

The markets hate uncertainty which is why the Pound has slid against the Dollar, no one knows what the future holds for the UK and how the departure from the EU will affect businesses based here in the UK. Whilst the (£) gained slightly last week when Theresa May said we wouldn’t bother with the EU at all – including customs union, single market etc. One feels it was more a relief of some discernible plan from no.10, rather than the riddle talking that had gone on previously.

The (£) itself is still well adrift of the highs of $1.50 > £1 that was achieved in the Summer of 2016 however.

It remains entirely unclear why some areas voted ‘leave’ other than for change. Areas like Sunderland which has benefitted hugely from the single market and customs union enabling Nissan to ship parts to Sunderland from the EU to produce their cars voting leave was surprising. Similarly Cornwall which benefitted hugely from subsidies and also EU money to build the airport still voted leave.

The uncertainty will continue as even with article 50 triggered, we’re entirely unclear what will happen, what deal will be struck and what the ambition of the EU is with their deal makers.

Brexit will fuel numerous things that feed economic elements that will impact all consumers in the UK, whether a Remainer, Leaver or undecided / not bothered. Everyone will feel the impact of subsequent inflation, potential for tariffs, jobs going abroad and heaven only knows what customs union changes….

It is difficult for retailers here other than making their voices heard and seeing what the future brings; there is a lack of exposure to Europe in terms of presence (bar Tesco). The future status of European workers in the UK will be a priority, but no retailer wants to be too ‘political’ here.

Alongside managing the uncertainty around the single market, the important aspect of the customs union and the ease of importing and exporting is also important. Any bureaucracy imposed here will lengthen supply chains, leading to more stock in transit and more working capital tied up, leading to potential availability challenges with price increases possible to offset the inefficiencies that any increased paperwork/delays would bring.

Quite the issue.

2. #inflation

Whilst Brexit is the main trend for 2017, the other trends for the year ahead are intrinsically linked. Inflation is always around, except when there is deflation which the UK briefly flirted with in 2016.

However the devalued sterling means that British companies buying products in USD($) or indeed other currencies find themselves having to spend more given the (£) being worth less vs. a ($) e.g. For exporters it’s the opposite – a weak pound makes it cheaper for others trading in their own currency to buy British.

However we import a lot of food, granted we do produce a lot within our own shores but we also import a good chunk via the EU. Just look at the Salads in Produce, Snow and Rain in Spain have decimated supply levels and there is barely a Courgette about in the Vegetable aisle.

Whilst British season will kick off in May, there is still a significant period of the year where we rely on imported fruit and vegetables to fill the shelves. Fresh foods aside; we know that a number of products come via expanded supply chains within the EU – the Unilever / Marmite situation showed us that products were produced over in Eastern Europe and then were shipped back into the UK for sale.

EU aside; importing other lines like Bananas and Sugar impacts the price at the shelf edge too, firstly the (£) is devalued so it costs more to get the same amount of Bananas and secondly, the volumes in which they’re sold means any ‘loss’ is multiplied significantly. So the price moves upwards instantly.

Hence why Bananas rose to 72p per kg and will likely rise again as buying agreements are re-negotiated and the currency weakness is exposed which in turn means someone has to pick up the slack – yes, it’s the customer.

There are numerous other categories where inflation will hit and it’s notable that stories about spending not being impacted are being held up as positive tales for Brexit, that we’ll be fine. We really haven’t seen anything yet.

Buying for Seasonal events like Halloween and Christmas for example will be happening now, if not already and with these lines bought in USD($) exposed to the lower (£) valuation – it means higher prices to UK customers, or less in the pack. Similarly electrical goods will be bought well in advance and the supply chains are set up to have stock in the pipeline at all times, as newer stock starts to arrive, bought at higher prices means that prices will rise here too.

It certainly will make for an interesting Black Friday in 2017.

Unless the supply chain / retailer can absorb the increase of course, however with slimmer margins in food post the ‘reset’ to combat discounters and support the rebasing of their model – they cannot absorb all cost increases.

Imported lines will cost more; that’s a given but some inflation will just be the market swinging back the other way. We can see that Dairy was at record lows in some cases for the past year or so, with Butter down at 82p in some cases – the market has corrected and these lines are now on their way back up. So whilst there is currency weakness and wider inflation via Brexit – in some cases the market is swinging back the other way too.

As ever, the Oil price fundamentally drives everything, and with Oil (Brent, Crude) at $55.45 a barrel on Friday, it’s been a steady rise with the price of a barrel as low as $44 in mid November. That translates into higher costs all round, particularly at the petrol pumps (more to come here)…..

Inflation is here to stay in the interim and the supply chains and retailers will do their level best to keep a lid on things, but no one is immune. Even discounters. That means – higher prices at the shelf edge.

3. #BenefitsFreeze

Despite the rhetoric from the government about how much they’re settled on focussing on those JAM’s and how hard life can be for them. There is still a benefits freeze in place until 2019 which will directly impact those consumers who are of eligible working age and receive benefits like Tax credits and Universal credit. Other benefits like Job seekers allowance, ESA (employment support allowances) and housing benefit are also frozen. Essentially some of the most hard pressed people in the country won’t see any rise in benefits until 2019.

Therefore where wages may rise, benefits are frozen and will not rise – therefore higher prices leaves those consumers very, very exposed indeed. Having to do more with less is near impossible and can only lead to a reduction in spending power for those consumers – this is bad news for retailers.

If you add in changes to the welfare structure that mean recipients of tax credits are being moved over to Universal credit, alongside the total benefits cap (£20k) – then it becomes even harder for consumers who are stuck in this bracket – whether they work or not, to maintain their standard of living without cuts of their own.

Consider that the majority of consumers will be saddled with debts of their own on credit cards that require servicing, making minimum payments still eats into budgets.

All roads lead to reduced spending power, which in turn means that retailers are exposed to lower discretionary spending and delivering higher prices due to inflation. Even though everyone needs to eat – this shift impacts all retailers, particularly non food operators alongside anything deemed not essential within the food space.

This is assuming that inflation doesn’t settle down, which given the ongoing uncertainty looks unlikely in the interim period.

This does bring opportunity for retailers; there is a reason why the FTSE250 post Brexit on 24th June saw the share price in Dominos tank. Customers will adjust their spending accordingly, and takeaway Pizza goes in favour of a similar treat, albeit one from a supermarket.

4. #LivingWage

This remains a concern for retailers given the rising costs elsewhere alongside a real level of uncertainty in the market along with inflation. It’s another area that has impacted consumers already of course, as retailers have adjusted their terms and conditions to facilitate the increase in hourly rates by adjusting premium payments, whether breaks are paid and also the loss of perks like a free meal in some companies.

Whilst the initiative was designed to improve living standards for ordinary people, a noble idea! The reality is that the government eyed this as a way to reduce the in work benefits by having employers pay their employees more as a minimum, again – very fair.

The mandatory wage rise is tiered until 2020 and will continue to impact profit margins in the retailers, private industry will never just ‘suck up’ such an idea without their own adjustments to make it as painless as possible to the bottom line.

Sub total? A broadly neutral pay position for the employees, where living wage means there’s a rise in the core hourly rate but a loss / flattening in premium payments and other ‘perks’ which will impact the overall financial package.

This is assuming that there isn’t any work undertaken by supermarkets to reduce their costs across their stores. There simply isn’t full time jobs created by supermarkets these days like there used to be, part time is the preferred option.

Discounters changed all this, recruiting colleagues on small contracts that offer guaranteed hours (6-9 per week fixed); with any extra made up by overtime as / when it’s available.

Should the store be busy, then overtime is readily available but workers taking holidays and/or sick are only paid for their base contract which is low – 6-9 hours per week. This means that discounters can control their costs and use overtime when necessary but not be lumbered with a high fixed cost on labour, year round.

If any retailers look to change terms and conditions of contracts to reduce their fixed costs and thus hours / shift patterns for colleagues in store, there would be a lump sum payment to facilitate such a change and ‘break’ the contract, but ultimately, the core earnings would then reduce.

We have seen shifts by Tesco to cease night shift operations in 100 stores due to low volumes and poor trading in affected stores. Meaning the store could be adequately filled on an evening / early morning, without the added expense of a night shift.

The impact to colleagues who stayed with the business was a payment to reflect a change in their terms and loss of role alongside staggered reductions in premiums. Ultimately – it leads to a lower wage given the absence of night shift payments.

This is partly due to the living wage, but also to do with the changing dynamics in the market. The discounters are low cost operators which keeps their prices low, which keeps the customers interested, Tesco have to compete somehow and growing sales and volumes is great news, but they (like others) have to reduce their cost base too.

Thus leaving the benefits system no better off despite the national living wage being introduced. Whilst the higher minimum wage is a great idea, private industry will never just suck up such a change and not make adjustments their end to minimise the impact, which we have seen.

Ultimately it would leave people earning at best the same wages, at worst less, if any such change in core hours/ change in shift patterns occurred and there was a reliance on overtime to make up the balance.

Not only that; but it would make calculating in work benefits like Tax Credit (> Universal credit) notably difficult given the variance in earnings, which would then feed in to over payments and hard pressed consumers having to pay back monies that were overpaid.

Thus feeding into a cycle of depressed earnings and impact on disposable incomes. Which affects the food retailers directly; given everyone has to eat – so these consumers have to shop somewhere…

Some of this is a future outlook given the highest wage level doesn’t become a reality until 2020, but there are staggered rises until then.

Any prospect of work based changes for consumers will impact confidence and reduce spending.

5. #Fuel

The big one is Fuel; and this would be a trend every year in reality, Oil prices have risen which has forced the price of goods up – nearly everything is affected by Oil of course.

Last year we had pump prices below £1 a litre for the first time since god knows when, however since those heady days, we are now seeing rise upon rise at the pumps and this causes real issues for food retailers firstly but all retailers in reality. Especially those out of town operators.

Firstly, increases in pump prices directly impact discretionary spending as the greater expense on Petrol means there is less money to go into shopping and the core budget.

We have seen retailers trying to keep a lid on rising prices but the advance buying means there is a level of volatility to the prices. Even the ending of the price (.9 typically) is now changing, with Asda and Morrisons operating at .7 and Sainsbury’s even operating at .4 and .2 last week.

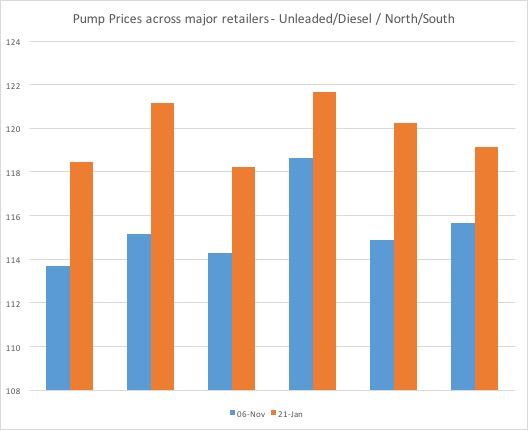

Research by Grocery Insight into pump prices (North / South) shows that from 6th November (1st week of tracking) to 21st Jan (week just passed), there has been a steady rise in fuel prices…

(data collected in the North/South and also the chart shows average prices, unleaded and diesel inclusive on a per litre basis, ‘major retailers’ are Asda, Morrisons, Sainsbury’s, Tesco, BP/Texaco and Shell forecourts).

With any fuel price rise felt immediately by consumers, it starts to impact budgets quickly. Secondly it also impacts where the consumer shops, and this decision will be based on their value perception but also the location of a store.

Out of town stores that require a longer journey may find themselves out of favour with shoppers who could literally be reviewing how full the petrol tank is before working out where they can afford to go and shop. This puts convenience stores in favour as they are local and also enable the customer to operate a tighter budget given the ability to visit this store daily if in close proximity.

Similarly discounters, who operate stores in all manner of areas do have stores that operate in the convenience realm given their neighbourhood based locations in some cases and smaller store footprint. Discounters also facilitate tighter budgeting given the low price and low choice model (despite increased ranges from Aldi)>

Larger retailers have done a lot of work on reshaping their model to mimic that of discount with an appreciation for a more rounded price package, not just ‘hi/lo’ promotions with poor value elsewhere. One thing is clear, if a customer makes a trip to an out of town, larger outlet – the retailer must be near A1 in terms of standards and availability.

Nothing worse for a customer on a tight budget and low fuel to make a trip out of town store to find the Nappies out of stock and queues aplenty at the checkouts.

Fuel prices are always important but with rising prices and a near perfect storm of stagnant income, in work benefits frozen and inflation coming up on the rails, they’re set to become ever more important in the year ahead.

#Conclusion

Whether you voted leave or remain; all consumers will be directly impacted by the decision to leave with inflation coming through in 2017, we have already seen several examples of this in the market.

Core staples will be affected; be it deflation swinging back the other way or higher import costs due to the weakened (£) affecting the exchange rate, value will become harder to seek out.

If prices don’t rise, then ‘shrinkflation’ will occur, where pack sizes adjust downwards to maintain the price point. However the consumer still loses out, as they’re paying the same price for less.

Similarly, longer term promotions may be tweaked to maintain a level of margin for the supplier and the retailer – instead of 6 yoghurts for £3, it may quietly change to 5 yoghurts for £3.

The winners in the market will be shaped by those who can best keep a lid on inflation, which is a hard task given the uncertainty in the market that affects imported products alongside home grown products. Larger suppliers like Unilever are also aware of the weakened (£) so don’t want their core business (reporting in EUR) to be impacted, hence price rises.

Single price(*) retailers like Poundland did rather well in the last downturn, as they offer a level of stability on prices and can also offer lines in affected commodity groups – like Coffee. Variety retailers like B&M and Home Bargains are strong in this arena too, however the increased non food exposure does leave them vulnerable to the currency weakness, putting pressure on already tight margins.

Further lines are being added at multiple price points in Poundland to maintain value and drive margins, with the retailer now privately owned by Steinhoff who have a number of interests around the world. It will be interesting to see if there is a trend towards single price / variety retailing once more.

It’s a mighty ask for both retailers and suppliers to bridge the inflation gap and not erode price perception though.

Managing inflation is one thing, and the retailers will collectively do a good job here given the competitiveness of the sector. We have seen Tesco push back on Unilever famously, the Sunday Times had a tale of Nestle trying to push rises through on Nescafe amongst other lines, again retailers will not just lay down and accept this.

The concern is for those smaller, local producers. How will they be able to square that circle of managing cost increases whilst remaining competitive with their supply contracts, at their size?

But someone has to pay, and its inevitable that the consumer will face higher prices and/or poorer value in terms of reduced pack sizes or weaker multibuy promotions within the market.

As outlined; every consumer will be impacted to varying degrees but the hard pressed consumer will face real pressure on their budgets via inflation, rising fuel prices, uncertainty in work (no pay rise and questions over contracted hours / shift patterns) alongside in work benefits that don’t rise despite prices increasing.

Meaning the budget gaps open up and decisions have to be made about cutting spending accordingly, thus impacting the wider economy.

This is a lethal cocktail facing some consumers in the UK, and one that retailers should consider when building their promotional packages and reviewing their own value proposition in the year ahead.

It may well get easier eventually, one hopes so as the pain in the short term will certainly be felt across retail, but particularly by customers and particularly in food.

The pricing data collected by Grocery Insight will be available at some stage in early February, aggregated from visits since October 2016 across a sample basket of around 60 items. Pump prices are also tracked – to express an interest, please use the contact us page on the website.

Similarly Grocery Insight operate exhaustively in the food sector, visiting stores, utilising images to illustrate all manner of insights into the wider market, consumer trends and retailer performance amongst other things. Several reporting services and advisory packages are available and the sheer amount of insight available means any brief can be answered in our unique way.

Do get in touch to discuss, always happy to talk shop! Contact Us.